Article · Economy · 8 min read

CPP sold Nvidia all the way up — and it became its biggest stock anyway

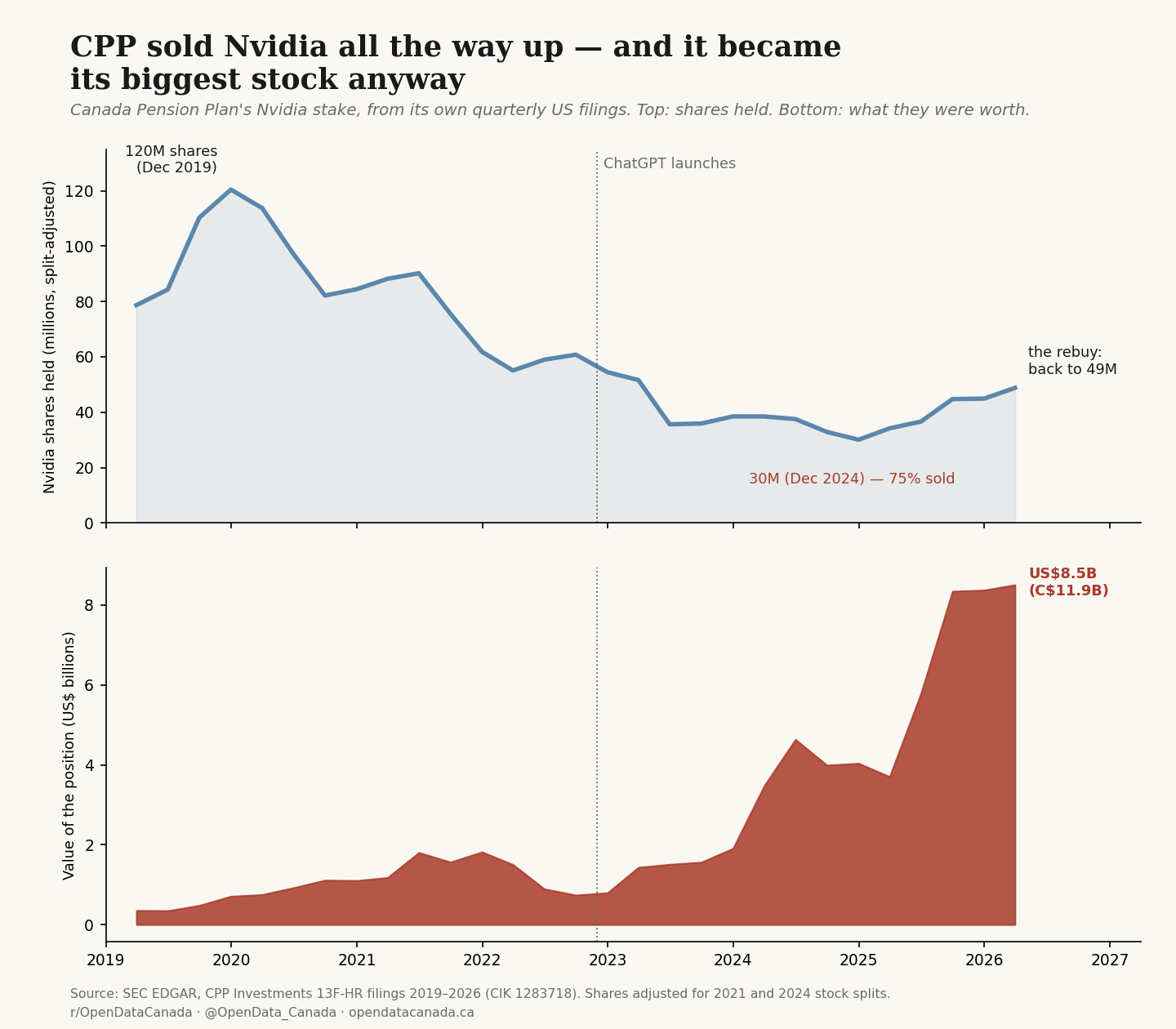

Before the AI boom, the Canada Pension Plan held 120 million Nvidia shares. It spent five years selling three-quarters of them — through the launch of ChatGPT, through the greatest stock run of the decade — then bought back in near the top. The shares it sold would be worth more than $15 billion today.

Every quarter, any institution managing more than US$100 million in US-traded stocks has to tell the American securities regulator exactly what it holds. CPP Investments — the fund behind the Canada Pension Plan, $793 billion as of March — is one of them. Line up its last twenty-nine quarterly filings and they tell a story about the single best trade of the decade: CPP had it, sold most of it, and ended up with it anyway.

Act one: they were early

At the end of 2019 — three years before ChatGPT, when Nvidia was still mostly a gaming-chip company — CPP held what is today the equivalent of 120 million Nvidia shares. By March 2020 the position was about 2 per cent of its entire US stock book. Nobody stumbles into a 2 per cent position; that's conviction. Whatever CPP's equity team saw in Nvidia, they saw it before almost everyone.

Act two: they sold it. For five years.

Then, quarter after quarter, the filings show the stake shrinking: 113 million split-adjusted shares in March 2020, 88 million a year later, 55 million by March 2022. When ChatGPT launched in November 2022 and the AI race began in earnest, CPP didn't stop — between that quarter and mid-2023 it cut the remaining stake by a third. By December 2024, the position bottomed out at 30 million shares. Three-quarters of the original stake, sold into the greatest single-stock run of the decade.

Act three: the rebuy

Here's where it stops being a story about discipline. Through 2025 — with Nvidia at the highest prices in its history — CPP started buying again. From the 30-million-share trough, the stake grew 62 per cent in five quarters, back to 48.8 million shares by March 2026. The Q1 2025 filing implies a Nvidia share price around US$108; by the Q1 2026 filing it was US$174. CPP sold for years at far lower prices, watched, and re-entered high.

And the punchline, visible in the bottom panel of the chart: none of the selling mattered. Nvidia's price rose so much faster than CPP could sell that the stock went from 0.7 per cent of its US book in 2019 to 5.5 per cent in 2026 — its largest single stock holding — across five years of near-continuous selling. CPP couldn't sell Nvidia fast enough to not own it.

Is that actually bad?

Here's the fair version. Pension funds are supposed to sell winners. A single stock growing into 5 per cent of the book is concentration risk; trimming it is rebalancing, not error, and every dollar of Nvidia sold went into something else that earned returns. If Nvidia had stayed collapsed after 2022 — CPP's own filings imply the share price fell from US$29 to US$12 between late 2021 and fall 2022, and the fund kept selling through that decline too — the same trims would look prescient. Counterfactuals built on the best-performing stock of the decade are rigged by construction: nobody writes this article about the stocks CPP sold that went nowhere.

But two details resist the charitable reading. The first is the rebuy — a disciplined rebalancer doesn't sell 75 per cent of a position and then rebuild it 62 per cent bigger at all-time highs. That pattern looks less like policy and more like conviction arriving after the move, which is the expensive time for conviction to arrive. The second is what the rest of the book did at the same time.

Meanwhile, the whole system bought the AI trade

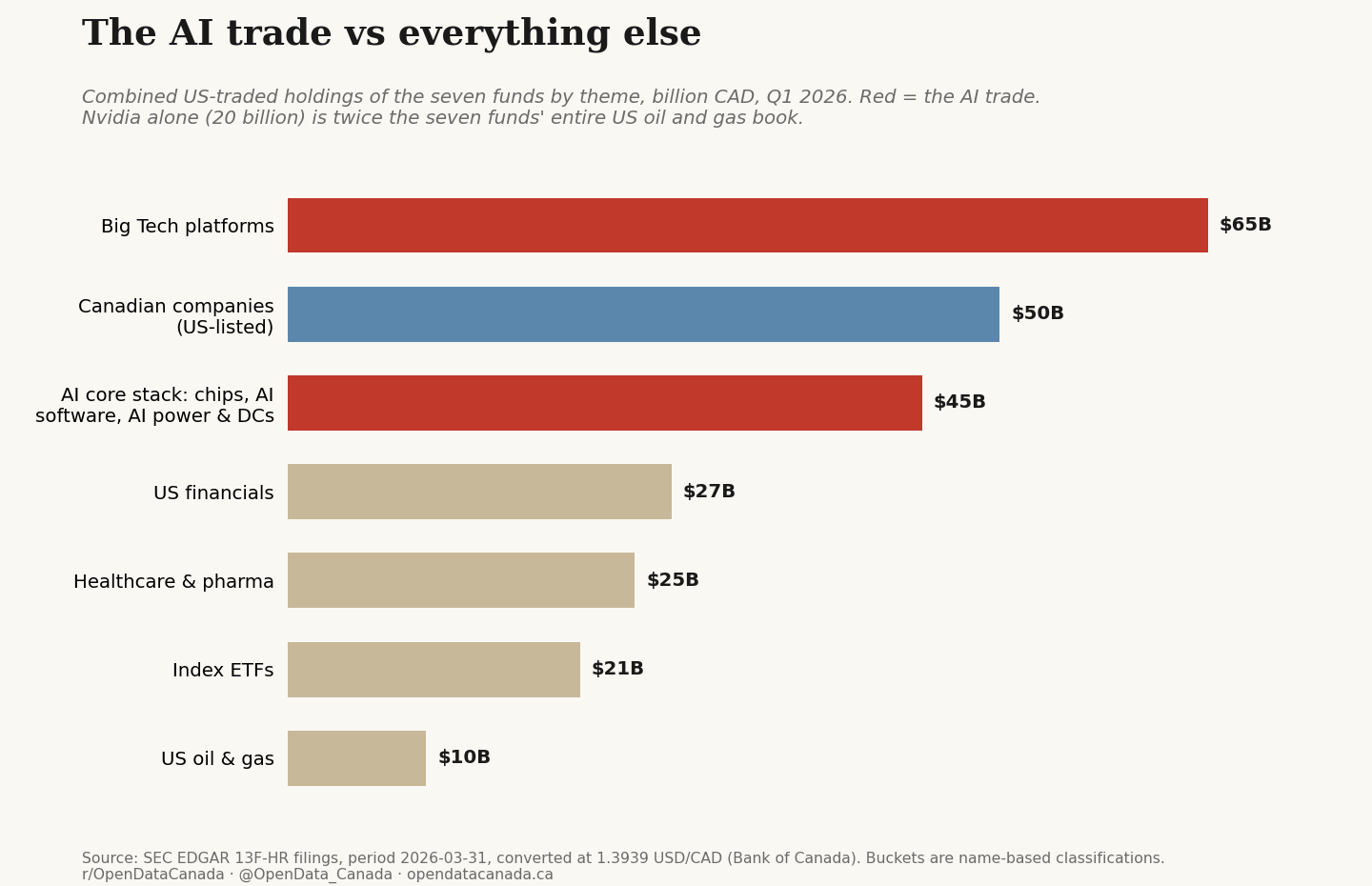

Pull the same filings for all seven of Canada's pension giants — CPP, Ontario Teachers', CDPQ, OMERS, BCI, PSP and AIMCo, roughly $2.5 trillion under management — and the AI bet is the book. The core AI stack alone (chips, AI software, AI-driven power and data centres) is $45 billion: bigger than the funds' combined US financials, bigger than their healthcare, and nearly as big as every Canadian company in their US filings put together. Count the Big Tech platforms whose capex is the AI buildout and the trade reaches $110 billion — 26 per cent of everything the seven funds disclose. Nvidia alone, at $20 billion combined, is twice their entire US oil and gas book.

There's even a second-order bet hiding in the data: more than $6 billion across Constellation, Vistra, Talen and GE Vernova — power companies whose story is selling electricity to data centres. Canada's pension funds aren't just betting on AI; they're betting on AI's power bill.

The private side points the same way. CPP has invested in both Anthropic and Cohere — backing two competing AI labs at once, an unusual move that drew notice in venture circles. PSP Investments, the fund for federal employees, the RCMP and the Canadian Forces, co-led Cohere's US$450–500-million Series D alongside Nvidia, Salesforce and Cisco — Canada's flagship AI company is part-owned by the federal workforce's pension. And Ontario Teachers' venture arm holds Databricks and Anthropic, plus exposure to Musk's xAI through its SpaceX stake — the same stake we covered earlier this week.

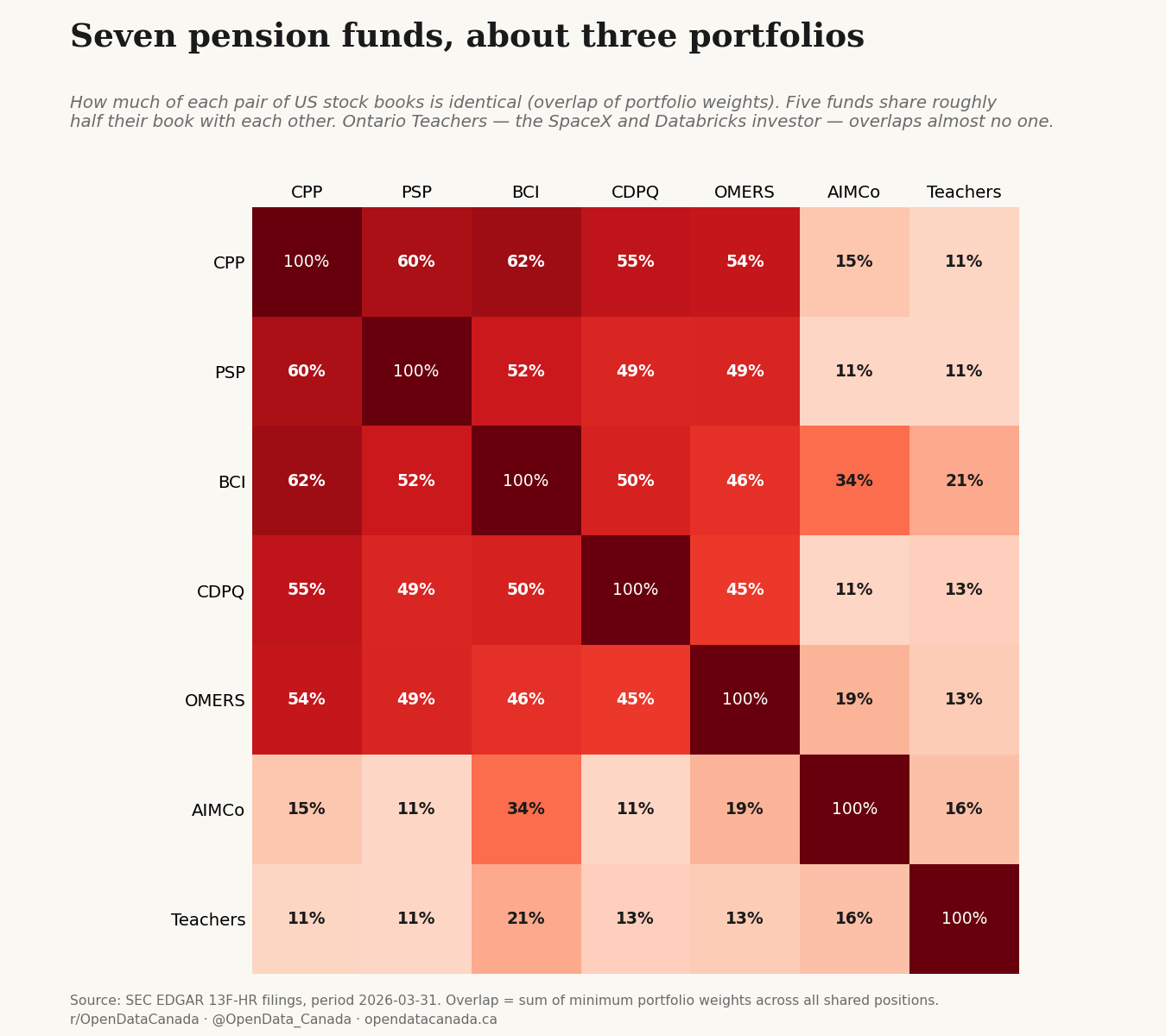

Seven funds, about three portfolios

If seven independently governed funds in five provinces all arrive at the same trade, are they really seven funds? The filings let us measure it: for each pair of funds, how much of their US books are literally the same positions at the same weights.

Five of them — CPP, PSP, BCI, CDPQ, OMERS — share roughly half their book with one another. Functionally, that's one big consensus portfolio with five letterheads. AIMCo sits apart mostly because its biggest US-filing positions are index ETFs. The genuine outlier is Ontario Teachers': 159 positions (CPP has 1,672), 65 per cent of its book in its top ten, and an 11-to-21-per-cent overlap with everyone else. Whatever you think of Teachers' bets — and its US-filing book is led not by Nvidia but by GFL Environmental, a Vaughan waste hauler — it is the only one of the seven making meaningfully different public-market decisions.

What to take from the filings

One. CPP's Nvidia history is the decade's cleanest case study in how institutions handle a monster winner: early conviction, years of policy-driven selling, and a late rebuy once the trade became consensus. The foregone ~$17 billion is a hindsight number — but the rebuy at the top is harder to file under discipline.

Two. A quarter of everything Canada's pension funds disclose in US filings is now one theme. If the AI trade keeps working, Canadian retirements are leveraged to it; if it unwinds, the same filings will show seven funds discovering the exit at the same time — because, mostly, they're in the same positions.

Three. The system's diversity is thinner than its org charts suggest. Five funds run half-identical stock books; one buys ETFs; one — Teachers' — actually runs a different portfolio. For a country that prides itself on the "Canadian model" of independent pension management, the filings show a lot less independence than advertised.

Caveats worth taking seriously

13F filings cover US-traded long positions only — no TSX listings, no bonds, no derivatives detail, no private assets — so they show each fund's US stock book, not its whole portfolio (for CPP that's 27 per cent of the fund; for Teachers', 2 per cent). Share counts are quarter-end snapshots; intra-quarter trading is invisible. We split-adjusted Nvidia's 2021 (4:1) and 2024 (10:1) splits and verified every Nvidia line in the pivotal filings is common stock, not options. The foregone-value figure assumes the December 2019 share count held untouched to March 2026 at the Q1 2026 filing's implied price, and ignores both the returns earned on redeployed proceeds and the dividends along the way. Theme buckets are name-based classifications. The Anthropic, Cohere and Databricks stakes are as reported by the funds and contemporary coverage; private positions don't appear in 13F data and their sizes are mostly undisclosed.