Article · Economy · 6 min read

Ontario Teachers invested early in SpaceX. The pension still trailed its benchmark and the S&P 500 in 2025.

Ontario Teachers' Pension Plan bought into SpaceX in 2019, and the stake could be worth as much as 11.6 billion U.S. dollars if the company lists at its targeted valuation. Yet in 2025 the fund returned 6.7 percent — below its own 11.7 percent benchmark and less than half the S&P 500's 17.9 percent. Its private equity lost money for the first time in 16 years. A look at what the windfall hides, and how Canada's pension giants are quietly changing what they invest in.

The headline writes itself. Ontario Teachers' Pension Plan — the fund that pays the retirements of roughly 346,000 working and retired Ontario teachers — put about 220 million U.S. dollars (roughly 300 million Canadian dollars) into SpaceX in June 2019, when Elon Musk's rocket company was valued at around 33 to 36 billion U.S. dollars. Musk is now steering SpaceX toward a public listing at a targeted valuation of 1.75 trillion U.S. dollars. If that holds, the slice Teachers bought in 2019 could be worth as much as 11.6 billion U.S. dollars — what the fund's own executives have called a "home run," and what would be the single most lucrative investment in its history.

That is the story that ran in the Globe and Mail, Bloomberg, and a dozen reprints. It is also the least interesting thing in Ontario Teachers' 2025 results.

Because in the same year that the SpaceX windfall came into view, the fund had a distinctly ordinary year — and on the measures a pension is supposed to be judged by, a poor one. Ontario Teachers returned 6.7 percent in 2025. Its own benchmark — the yardstick it sets for itself — returned 11.7 percent. That gap is worth roughly 12 billion dollars of value the fund did not add. And a teacher who had simply held a plain U.S. index fund would have done far better: the S&P 500 returned 17.9 percent in 2025, and the S&P/TSX 60 in Canada returned 29.1 percent. Those last two figures are not our characterization. They are printed in Ontario Teachers' own annual report.

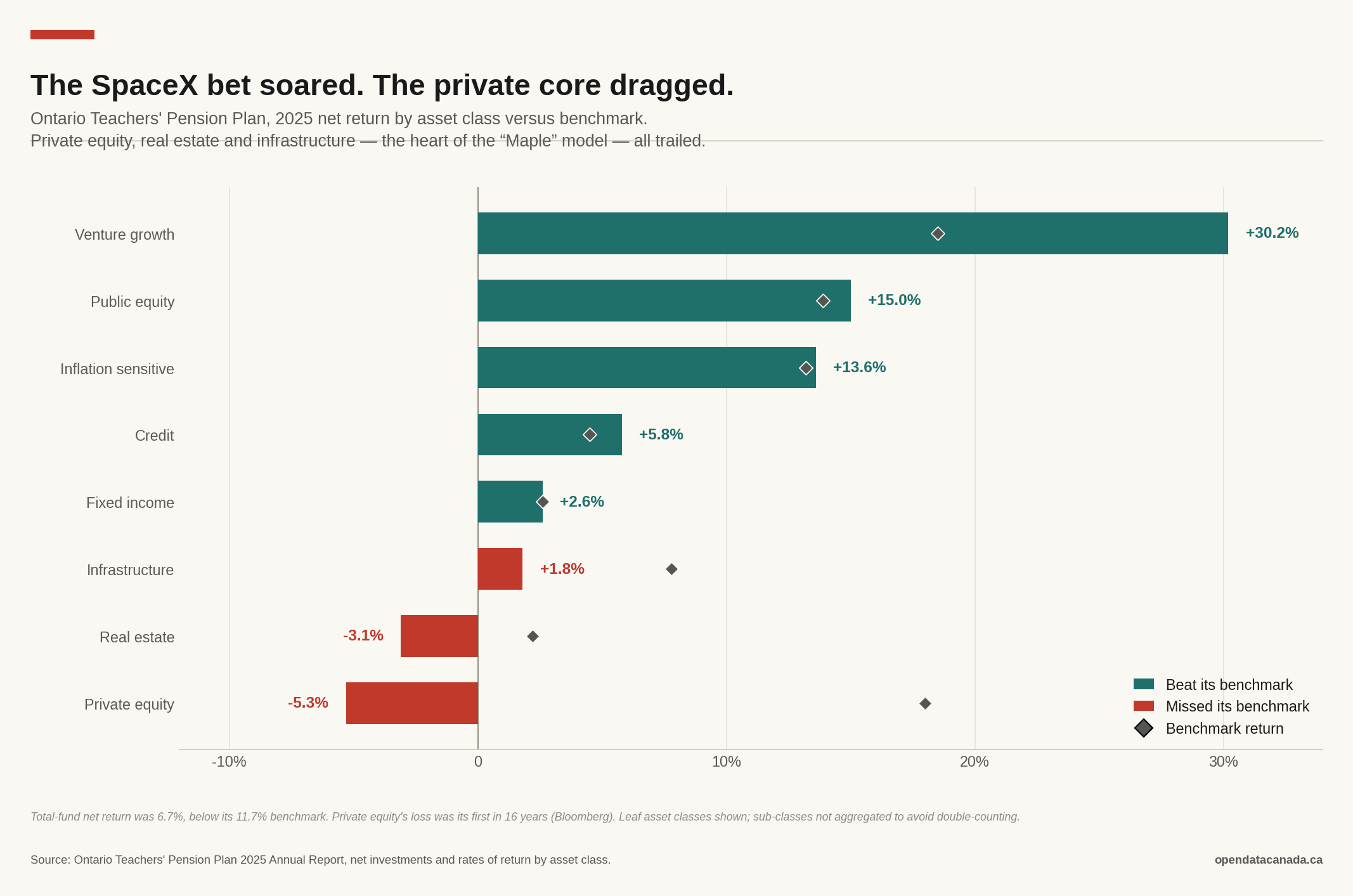

The SpaceX bet soared. The core dragged.

Pull the year apart by asset class and the picture sharpens. The pieces of the fund that did well in 2025 were the liquid ones and the new ones. Public equity — ordinary listed stocks — returned 15.0 percent. Venture growth, the small, fast-moving arm that holds SpaceX, returned 30.2 percent, its report crediting "strong valuation gains across several high-performing assets, in particular SpaceX and Databricks."

What dragged was the private core — the buyouts, buildings and toll-road-style assets that are the signature of the so-called "Maple" model that made Canada's big pensions famous. Private equity lost 5.3 percent, its first annual loss in 16 years, according to Bloomberg. Real estate lost 3.1 percent. Infrastructure returned just 1.8 percent against a 7.8 percent benchmark — a six-point miss on a 34.5 billion dollar book.

The single most striking bar is private equity: a 5.3 percent loss against a benchmark that returned 18 percent. The most lucrative investment in the plan's history fired, and the fund still could not reach its own target.

In fairness to Ontario Teachers

A pension is not a hedge fund, and beating the S&P 500 in a single year is not its job. Its job is to pay a defined benefit to teachers for decades, with as little volatility as possible. Trading some upside for stability is the entire point of holding private assets that do not swing with the daily market.

And there is a mechanical reason a private-asset-heavy fund lags in a year when public markets surge. Private holdings are valued infrequently, by appraisal, so they do not capture a public-market rally in real time. Ontario Teachers makes exactly this argument in its report: the benchmark shortfall, it writes, "is consistent with periods of strong public market performance, as private assets … typically generate more stable and less volatile returns over time."

The five-year numbers give that defence some support — and complicate it. Over five years, private equity returned 8.4 percent annualized: positive, respectable, not a failure. But over that same five years, public equity returned 10.0 percent — so the cheap, liquid option still edged the expensive, private one. Real estate, meanwhile, is not a one-year problem: it has lost 2.2 percent annualized over five years. The total fund's five-year return of 6.6 percent also sits below its 8.8 percent benchmark.

So the fair reading is not that the model is broken. It is that 2025 was the kind of year that tests it — and that even a generational win on SpaceX could not paper over.

Canada's pension giants are changing what they invest in

The SpaceX bet is not a one-off. It is the emblem of a shift underway across Canada's largest pensions in what, and how, they invest.

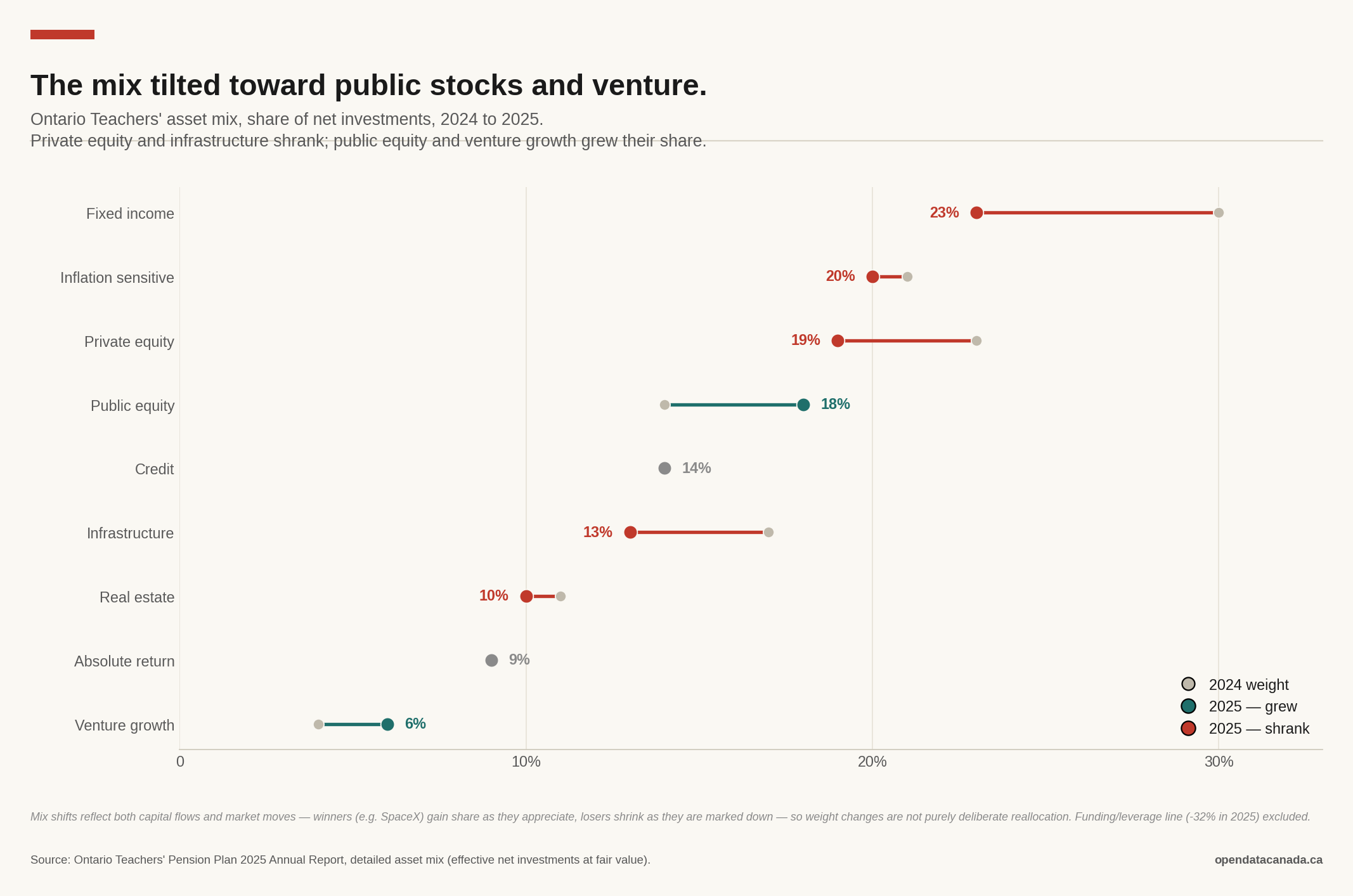

Ontario Teachers created the venture arm that holds SpaceX — Teachers' Venture Growth — only in 2019, to chase late-stage technology companies. By the end of 2025 it had grown to hold not just SpaceX but Databricks, the AI company Anthropic, the data firm Quantexa, the energy retailer Octopus Energy and others. Its share of the fund rose from 4 percent to 6 percent in a single year. Public equity's share rose too, from 14 to 18 percent. Private equity's share fell from 23 to 19 percent, and infrastructure's from 17 to 13.

A caution on that chart: not all of the shift is a decision. When SpaceX's value rises, it takes up a bigger slice of the fund without anyone buying more of it; when private equity is marked down, its slice shrinks on its own. So the mix tilting toward public stocks and venture reflects both choices and market moves.

But the choices are real, and they are industry-wide. Across the "Maple Eight" — the country's largest funds, which together hold more than 400 billion dollars in private equity — the trend is to pull back from doing private-equity deals directly and instead invest through established firms such as Blackstone and KKR, and alongside other big investors. CPP Investments recently sold a portfolio of 25 private-equity fund stakes. Several Canadian pension funds have signalled interest in financing AI data centres. Meanwhile, the office real estate that funds loaded up on before the pandemic keeps getting written down. This is not a wholesale exit from private assets — they remain roughly a fifth of these funds' holdings — but it is a real change in style: lighter on direct deals, heavier on partnerships and on technology.

The catch in the windfall

There is a final irony worth holding onto. The 11.6 billion dollar SpaceX figure is a projection, not a cheque. It assumes SpaceX lists at 1.75 trillion dollars, assumes the 2019 stake was never diluted, and counts only that original tranche. SpaceX has not gone public. And Ontario Teachers' own investment chief, Gillian Brown, has said the IPO is "not necessarily a target exit point" — the fund may well keep holding.

Which means the pension's biggest paper gain is, for now, exactly that: paper. It is a large, concentrated, illiquid position the fund cannot easily turn into pensions — the same illiquidity that just bit its losing private bets, only on the winning side. The teachers' retirement is, in a small but real way, riding on Elon Musk's space company, which in the past year also absorbed his artificial-intelligence venture, xAI.

Why it matters

Canada's pension funds are a genuine national achievement, copied by governments around the world for their scale and their in-house management of private assets. That model just had a year in which its private core lost money, plain public stocks beat it, and the fund missed its own benchmark by about 12 billion dollars — all while sitting on the most celebrated single investment in its history. None of that means the model has failed. It does mean the test is real, and that the way these funds invest is shifting under it. For the teachers whose retirements depend on the answer, that is worth more attention than the rocket.