Article · Economy · 7 min read

We compared all of Canada's pension giants. The one that beats its own benchmark by the widest margin isn't the famous one.

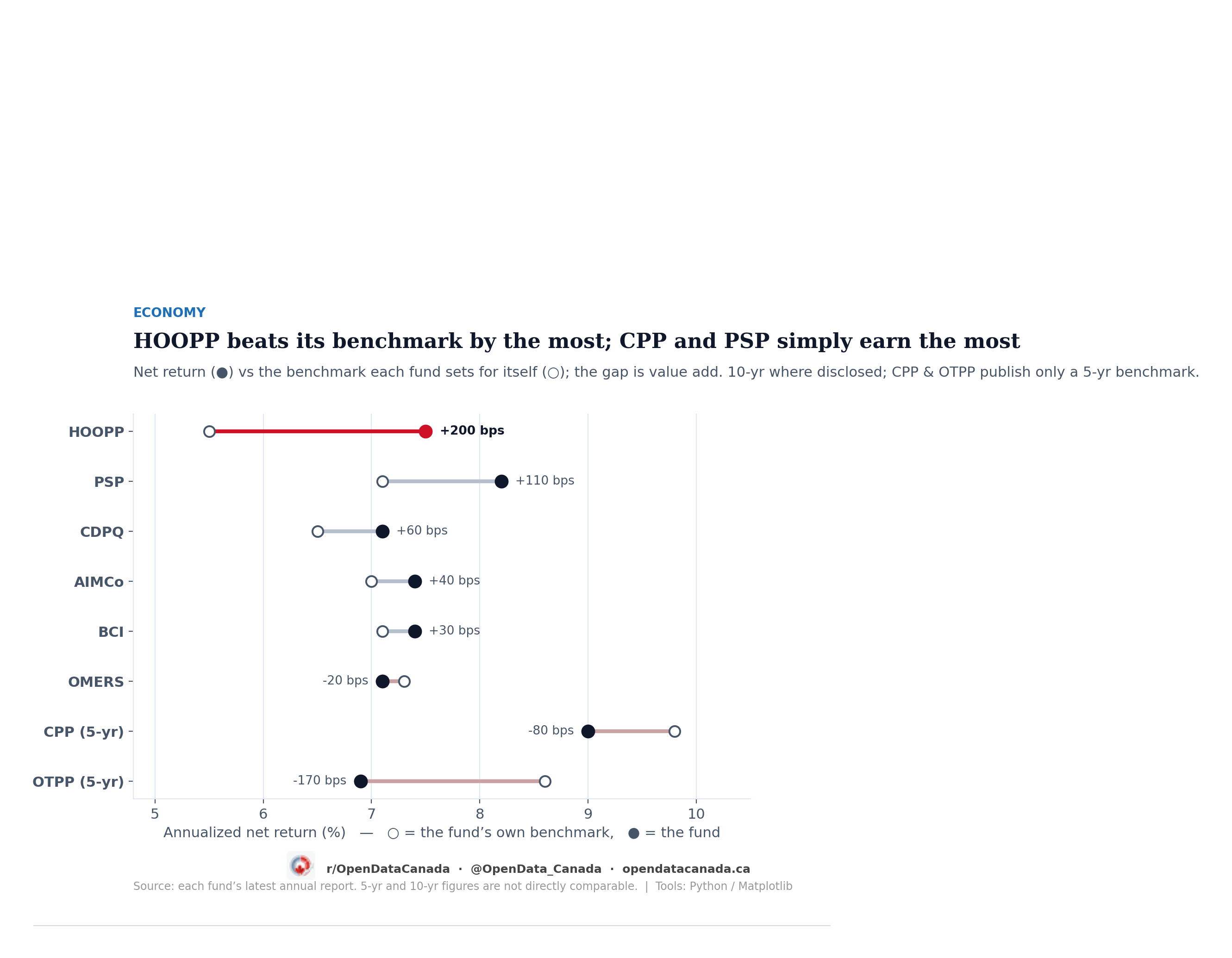

After Ontario Teachers trailed its benchmark, we pulled the latest annual report of all eight of Canada's pension giants and built one standardized scorecard. Over a decade, only HOOPP clearly beats the benchmark it sets for itself — by 2 full percentage points a year. CPP and PSP earn the highest raw returns. And on the question that started this — private companies — almost no fund reliably beats its own private-equity benchmark once you stop looking at a single year.

Earlier this month we wrote about Ontario Teachers' Pension Plan, which got into SpaceX early and still trailed its own benchmark in 2025, with its private equity posting a loss for the first time in 16 years. The obvious next question came back from readers almost immediately: fine, but who's actually good at this? If a teacher, a nurse or a federal employee can't pick their fund, which of Canada's pension giants is the best — and which is best at the private-company bets these funds are famous for?

So we pulled the most recent annual report from all eight of the funds usually grouped as Canada's "Maple Eight" — CPP Investments, the Caisse (CDPQ), Ontario Teachers', PSP Investments, British Columbia's BCI, OMERS, Alberta's AIMCo and HOOPP — and built a single scorecard. No one publishes one: each fund reports on its own terms, in its own fiscal year, against a benchmark of its own design. Assembling the comparison is the work, and so is being honest about where it breaks down.

How to keep score without fooling yourself

The wrong way to do this is to line up last year's returns and crown a winner. A pension's job is not to win a year; it is to pay a defined benefit for decades. And a single year of outperformance can be pure luck — the way roughly half of all fund managers "beat the market" in any given year for no reason other than a coin landing their way.

So we judge two things, both the way the funds ask to be judged. First, value add: a fund's net return minus the benchmark it sets for itself, measured in basis points (100 basis points is one percentage point). This is the honest answer to "could you have just bought the index?" — because the benchmark is a passive version of the fund's own strategy. Second, we use the longest window each fund discloses — ten years where we can, five where that's all there is — because that is long enough for skill to start outrunning luck. Where a fund earns a high return only by taking more risk, beating its own risk-matched benchmark is what separates the two.

The fund that beats itself by the most is the quiet one

On value add over the long run, the order is not the one the headlines would predict. The Healthcare of Ontario Pension Plan — HOOPP, which manages 123 billion dollars for Ontario's hospital workers and rarely makes news — beat its own benchmark by about 200 basis points a year over ten years (7.5% against 5.5%), and by 170 over twenty. No other fund is close on that measure. PSP Investments, the 300-billion-dollar manager for the federal public service, military and RCMP, is next at +110 basis points over a decade. The Caisse follows at +60.

After that the margins thin out fast. AIMCo and BCI cleared their benchmarks by 40 and 30 basis points over ten years — barely. OMERS came in 20 basis points under. And the two best-known names in Canadian pensions fared worst against their own yardsticks: Ontario Teachers trailed its benchmark by about 170 basis points a year over five years, and CPP Investments — at 714 billion dollars, by far the largest — trailed its own five-year benchmark by roughly 80. The biggest fund in the country, run almost entirely in-house at considerable cost, did not beat the passive portfolio it measures itself against.

"Best" depends on which question you're asking

Value add is the fairest single test, but it is not the only one, and it would be cherry-picking to stop there. Ask instead which fund simply made the most money, net of fees, and the ranking flips at the top. On raw ten-year return, CPP leads at 8.3% a year, with PSP just behind at 8.2% — both ahead of HOOPP's 7.5%. CPP trails its own benchmark, but its benchmark is a demanding one; in absolute dollars its members did well.

That tension is the real answer to "who's best." HOOPP is best at the narrow job of beating the bar it sets for itself, and it does so with a famously cautious, liability-matched book. CPP and PSP put up the highest raw numbers. They are different definitions of good, and a fund can satisfy one without the other. What none of the eight did was both clear its benchmark by a wide margin and top the raw table — there is no free lunch hiding in these reports.

Who is actually best at private companies

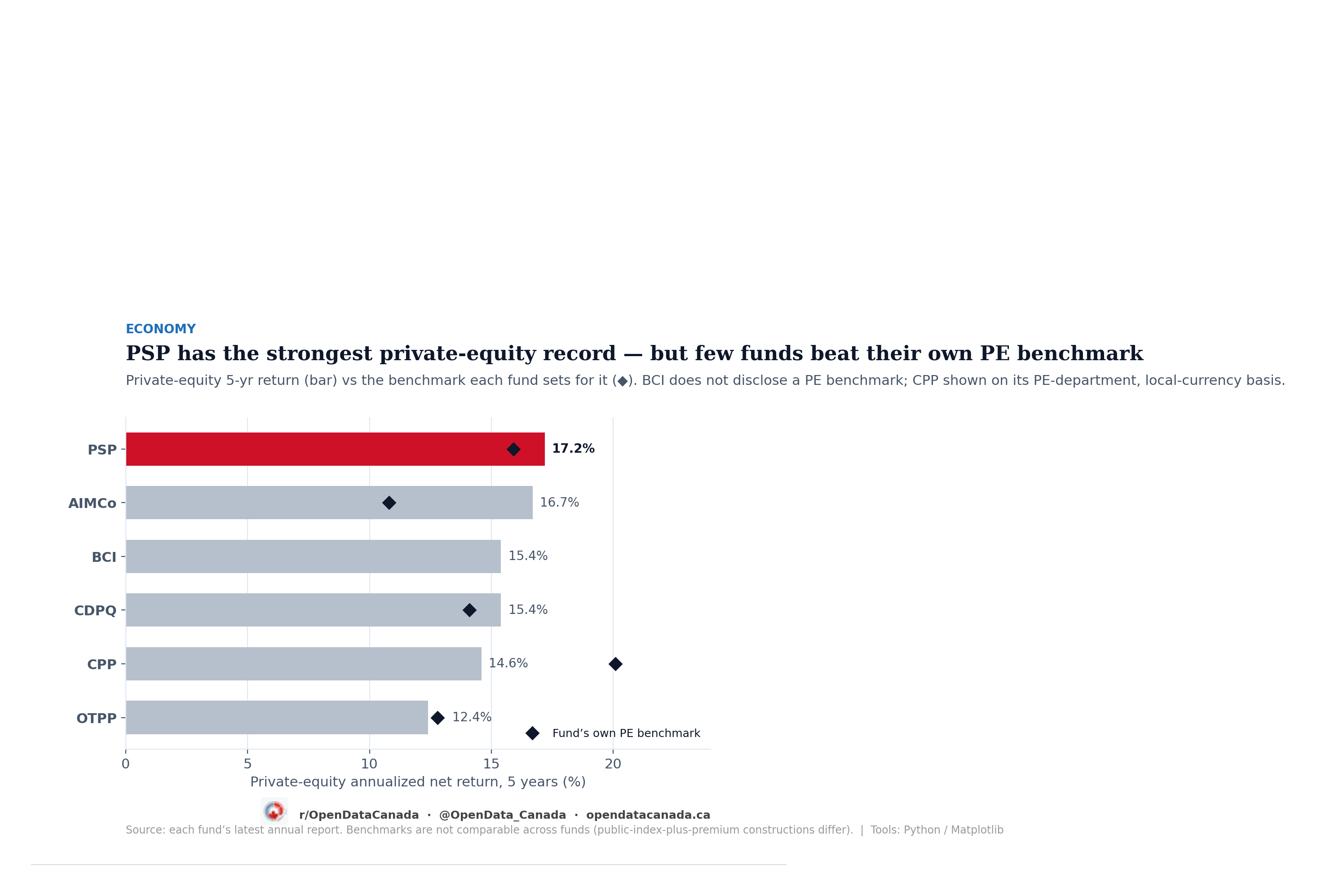

The bet that started all this was a private one — Ontario Teachers' stake in SpaceX. Private equity, the funds' direct and partnered ownership of companies that aren't publicly traded, is the signature of the Canadian model. So which fund is best at it?

On the raw return, PSP has the strongest private-equity record: 17.2% a year over five years, with AIMCo close behind at 16.7% and the Caisse and BCI at 15.4%. Ontario Teachers, the fund with the celebrated SpaceX position, sits at the bottom of this group at 12.4% — a reminder that one famous winner is not a portfolio.

But raw return rewards taking more risk, so the sharper test is again whether each fund beat the benchmark it set for its own private book. Here the picture is bleaker, and more interesting. Only a few funds cleared their private-equity benchmark over five years at all. AIMCo beat its by a large margin; PSP and the Caisse beat theirs by about 130 basis points each. CPP's private-equity arm trailed its benchmark by several hundred basis points. And the comparison can't be pushed too far, because these benchmarks aren't built the same way — AIMCo measures its private equity against world public stocks plus two percentage points, while others use different blends. A fund can look like a hero or a laggard depending on the bar it chose, which is exactly why we don't reduce this to a single league table.

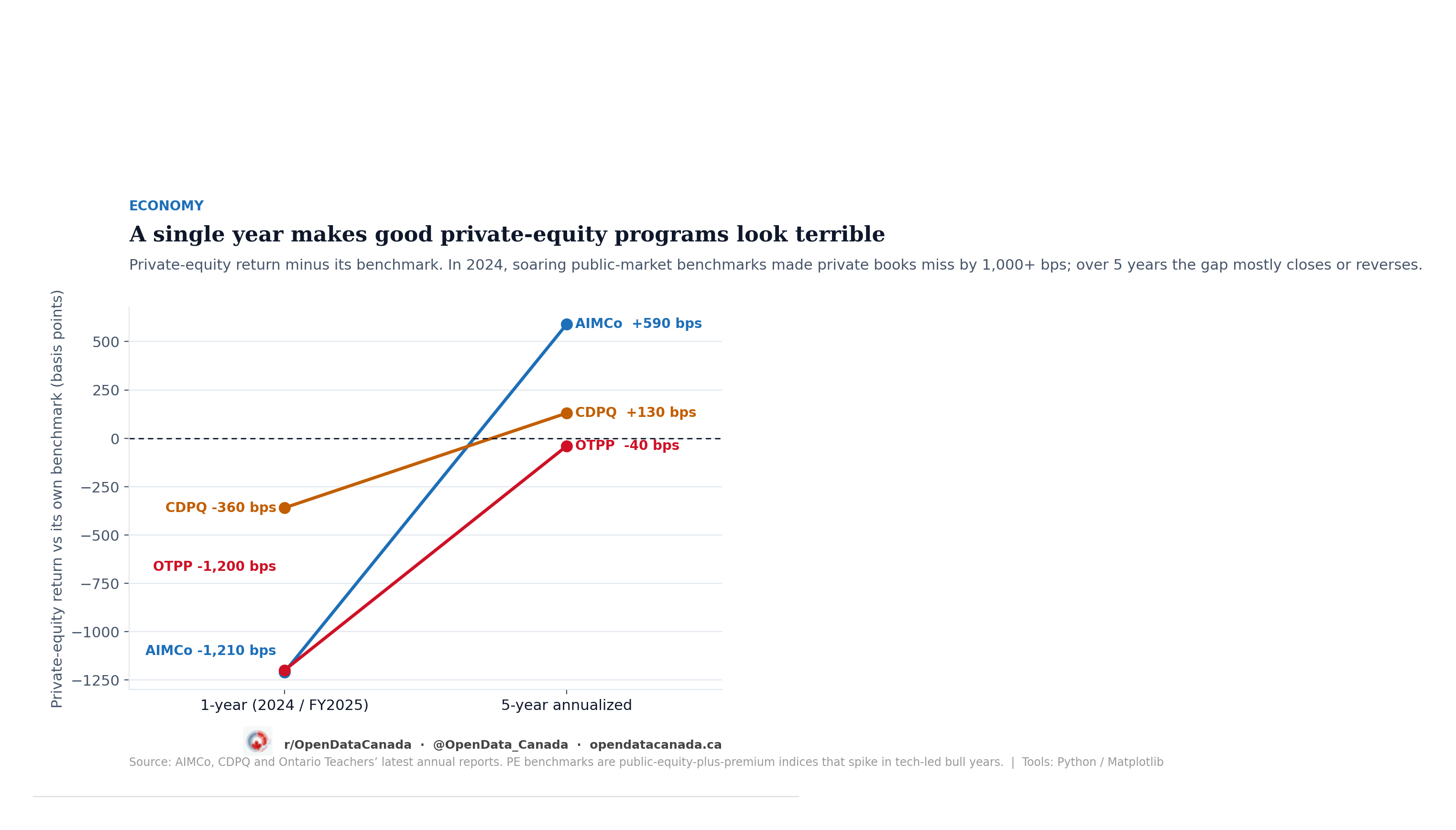

A single year lies — especially about private equity

There is one trap worth dwelling on, because it explains a great deal of the alarming numbers in these reports, including Ontario Teachers' 2025 loss. Private holdings are valued slowly, by appraisal, so they don't capture a public-market rally in real time. Their benchmarks, though, are usually built from public-market indices plus a premium — and those indices soared in the tech-led run of 2024. The result is a benchmark that sprints ahead while the private book is still being marked.

In the latest single year, Ontario Teachers' private equity came in about 1,200 basis points below its benchmark, and AIMCo's about 1,210 below. Read on its own, that looks like a catastrophe. Stretch the window to five years and AIMCo's private equity is ahead of its benchmark by 590, and Ontario Teachers' gap shrinks to a rounding error. The single-year number wasn't measuring skill; it was measuring the calendar. It is the same effect that made Ontario Teachers' 2025 look so much worse than its decade — and a good reason to distrust any pension ranking built on one year.

Why it matters

The loudest reaction to the first piece was a version of "so why not just buy an index fund?" Over one year in a roaring market, the index does win — that was the whole point of the SpaceX story. Over a decade, these funds returned between 7.1% and 8.4% a year net of all costs, through a pandemic crash and a bond rout, with far less volatility than a stock portfolio and a mandate to keep paying pensions either way. That is a different product than an index fund, and judging it by a single good year for stocks misses what it's for.

What the full scorecard shows is narrower and more useful than a champion. Beating your own benchmark over a decade is hard: most of Canada's giants barely managed it, two of the most famous didn't, and only one — the quiet hospital fund — did it convincingly. And the private-company investing these funds are celebrated for is, on the honest measure, rarely a clear win over the cheaper public version of the same bet. For the millions of Canadians whose retirements ride on these eight institutions, that is the part worth watching — not the rocket.