Article · Industry · 7 min read

Canada was the world's 4th-largest carmaker in 2000. It now ranks 14th — behind the Czech Republic and Turkey.

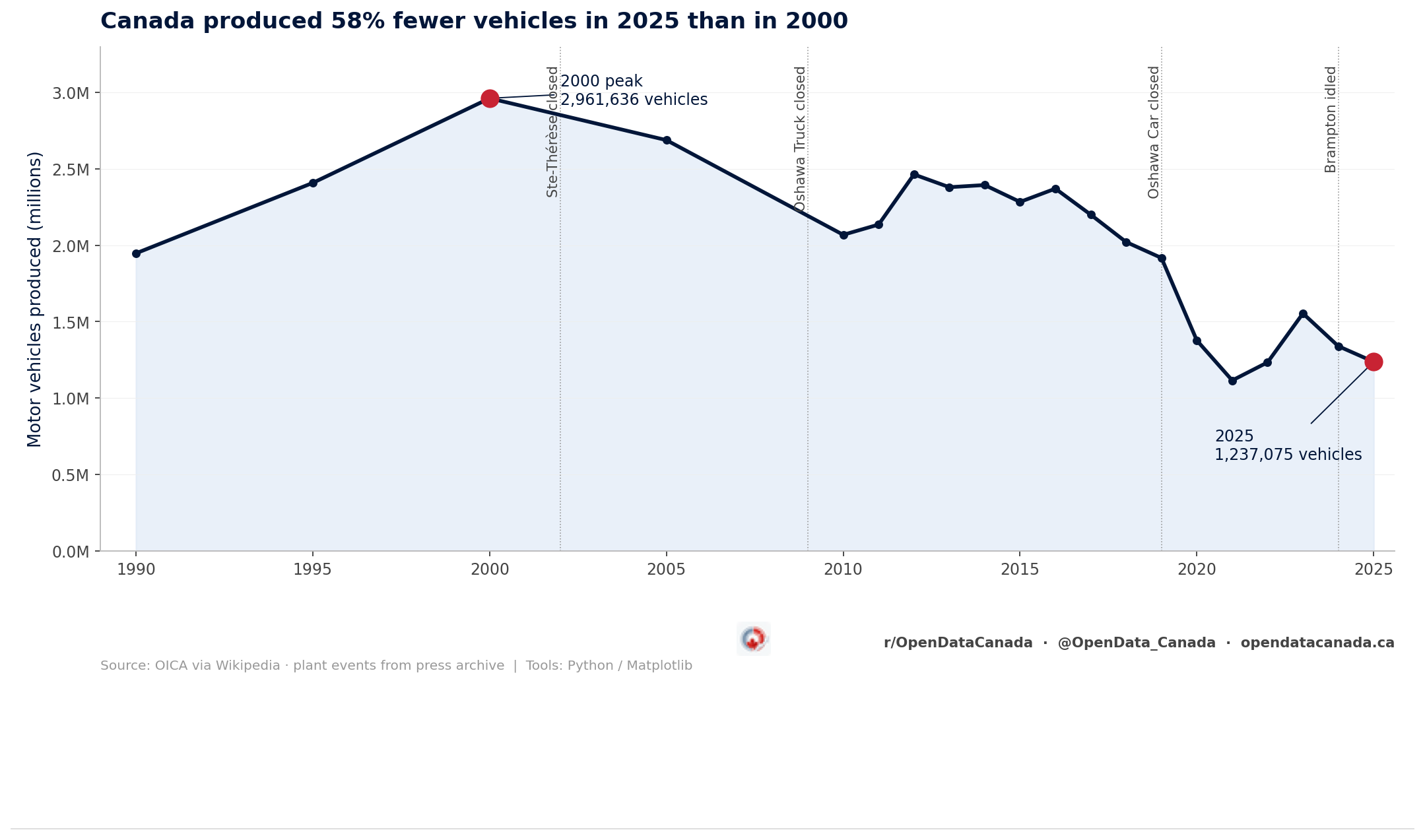

In 2000 Canada built 2.96 million motor vehicles and sat fourth in the world, behind the United States, Japan, and Germany. In 2025 it built 1.24 million and ranked fourteenth — behind the Czech Republic, behind Turkey, and a single year of catch-up behind Indonesia. Mexico, the country Canada used to outproduce, now builds 3.3 times as many vehicles as Canada does.

The 25-year slide

OICA's country production tables are the standard source for cross-country comparisons; Wikipedia's editors keep the year-by-year totals current as OICA publishes each annual release. The Canadian series in those tables runs continuously from 1950 onward; the verified subset below uses only the years Wikipedia and OICA agree on as of May 2026.

The decline is not a single drop. It is a step function with three notches.

| Period | Canada production | Notes |

|---|---|---|

| 1990 | 1,947,106 | Pre-NAFTA baseline |

| 1995 | 2,407,999 | NAFTA implemented Jan 1, 1994 |

| 2000 (peak) | 2,961,636 | Canada ranked #4 globally |

| 2005 | 2,687,892 | Post-NAFTA peak window closes |

| 2010 | 2,068,189 | Post-recession recovery to ~2/3 of peak |

| 2015 | 2,283,474 | Recovery flatlines |

| 2019 | 1,916,585 | GM Oshawa Car closure in December |

| 2020 | 1,376,623 | COVID + idling year |

| 2021 | 1,115,002 | Semiconductor shortage trough |

| 2023 | 1,553,758 | Brief rebound |

| 2025 | 1,237,075 | Brampton idle through full year |

The two largest single-year drops in the series are the 2009 collapse — global financial crisis, GM bailout, Oshawa Truck's last shift on May 14 — and the 2020 collapse driven by COVID idlings. The 2021 trough at 1.11 million was the lowest single year on record since at least 1970.

But the more important story isn't any one year. It is that production has not returned to the 2 million floor since 2019. Canada lost a million units of annual output in a decade and has not built them back.

The mechanism: four plant exits in 23 years

The decline lines up with assembly plants leaving Canadian soil. Four exits explain most of the lost capacity:

Sainte-Thérèse (Boisbriand), Quebec — closed September 2002. GM's Quebec assembly plant, which built the F-body Chevrolet Camaro and Pontiac Firebird, was suspended in September 2002. About 1,400 workers were laid off. The plant was later demolished. It was Quebec's last vehicle assembly plant.

Oshawa Truck Assembly — closed May 14, 2009. GM ended Sierra/Silverado production at its Oshawa truck facility on the same day GM filed for Chapter 11 in the United States. The last truck, a black 2009 GMC Sierra 1500 Crew Cab, was raffled off to an employee. The Canadian Auto Workers (now Unifor) negotiated a settlement that kept the Oshawa car plant alive — temporarily.

Oshawa Car Assembly — closed December 18, 2019. GM ended vehicle assembly entirely at Oshawa on December 18, 2019, after producing over 20 million vehicles since 1953. About 2,600 unionized assembly workers lost their jobs. The site was repurposed for parts production. A subsequent retooling allowed limited truck assembly to resume, but at a fraction of the original footprint.

Brampton Assembly — idled February 2024. Stellantis stopped production of the Dodge Charger, Dodge Challenger, and Chrysler 300 in December 2023 and idled the plant in February 2024 for retooling. Approximately 3,000 workers were laid off. Retooling work was paused around April 2025. As of April 2026 the plant has been idle for over two years with no firm reopening date; Jeep Compass production originally allocated to Brampton was redirected to Belvidere, Illinois.

The Honda Alliston decision in May 2026 — shelving the C$15 billion EV investment Canada had counted as the centerpiece of the next decade — and Ford Oakville's pivot away from the announced electric SUV program to F-Series Super Duty pickups represent the next chapter rather than the current one. Both decisions affect future production, not 2025's. But they are the same pattern: Canadian assembly capacity converted to something less, or postponed, or pulled across the border.

Same continent, opposite trajectory

The decline reads differently against Mexico. Both countries entered the North American free trade regime as junior partners to the United States. The crossover point is older than commonly remembered — Mexico passed Canada's annual vehicle output between 1990 and 1995 and has not been behind since.

| Year | Canada | Mexico | Mexico ÷ Canada |

|---|---|---|---|

| 1990 | 1,947,106 | 1,814,466 | 0.93× |

| 1995 | 2,407,999 | 2,629,008 | 1.09× |

| 2000 | 2,961,636 | 3,099,522 | 1.05× |

| 2010 | 2,068,189 | 3,981,728 | 1.92× |

| 2015 | 2,283,474 | 4,029,463 | 1.76× |

| 2020 | 1,376,623 | 3,176,600 | 2.31× |

| 2023 | 1,553,758 | 4,002,047 | 2.58× |

| 2025 | 1,237,075 | 4,092,448 | 3.31× |

Mexico's 2025 output is 4.1 million vehicles — higher than Germany, higher than South Korea, and roughly equal to South Korea plus the Czech Republic combined. Canada's 2025 output is below the Czech Republic on its own.

The driver is not subtle. Labour-cost arbitrage under USMCA, plus the regulatory and trade-policy uncertainty Canadian plants have faced through three federal governments, made Mexico the destination for new continental capacity. The U.S. side of NAFTA/USMCA did not crater — U.S. production also fell, from 12.8 million in 2000 to 10.2 million in 2025, a 20 percent decline. But the U.S. retained its top-3 ranking and absolute scale. Canada lost both.

The jobs picture — narrower than headline production

Statistics Canada's Table 14-10-0202-01 tracks employment in Motor Vehicle Manufacturing (NAICS 3361) annually since 2001. The series captures payroll employees at the assembly facilities themselves — not the parts ecosystem (NAICS 3363) or the dealer/wholesale chain.

| Year | Employees, NAICS 3361 |

|---|---|

| 2001 | 53,204 |

| 2005 | 51,808 |

| 2008 | 43,347 |

| 2009 | 36,317 |

| 2015 | 42,117 |

| 2018 (recent peak) | 44,747 |

| 2019 | 44,177 |

| 2020 | 36,304 |

| 2023 | 38,310 |

| 2024 | 35,933 |

| 2025 | 35,593 |

The 2025 figure of 35,593 employees is a 33 percent decline from 2001 and a 21 percent decline from the 2018 modern peak. The collapse is less dramatic than the production drop because productivity per worker has risen — modern lines build more vehicles per labour hour than 2000-era lines did. But the jobs number is also smaller than the production-share number suggests because the Canadian remnant is more capital-intensive and more concentrated: a few large facilities account for most of what remains.

What that means for policy: protecting the assembly sector with subsidies — Honda's announced C$15 billion EV investment was a federal/provincial commitment north of C$5 billion in incentives; Ford Oakville's F-Series Super Duty pivot was supported by C$464.5 million in federal funding announced in May 2026 — buys preservation of a much smaller employment base than the equivalent investment would have bought in 2000.

What the 2025 number does and doesn't tell us

Canada's 2025 production of 1.24 million is not a transient COVID-recovery number. The semiconductor shortage that drove 2021's 1.11 million floor is resolved. Demand for North American vehicles is not anomalously weak in 2025 — U.S. production at 10.2 million is within 4 percent of its 2023 reading. Canada's underperformance is structural.

Two readings of the immediate trajectory are possible.

The first is that 2025 represents a soft floor. The Brampton facility is still nominally retoolable for Jeep Compass or a successor EV; Ford Oakville will eventually return to full Super Duty volume; Honda's Alliston buildings physically exist and could be revived if the U.S. EV demand picture changes. On that reading, Canada's output stabilizes near 1.2–1.5 million and the ranking holds at #14–#15.

The second is that 2025 is the new equilibrium for an industry pulling back further. Honda's shelving of Alliston is the largest single Canadian auto investment cancellation on record. Ford Oakville moved from EVs to gas trucks — a downshift in long-run capacity. Brampton has been idle through two model years with no firm restart. On that reading, 2026 prints below 2025, Indonesia overtakes Canada, and the ranking slides to #15 or #16.

Either way, the headline doesn't change much. Canada is no longer a top-tier global producer. The country that built nearly 3 million vehicles in 2000 now builds fewer than the Czech Republic.